Co-buying a Home in 2021 Report

Co-buyers now make up 25% of all home-buyers across the U.S. So why are co-buyers still underserved and misunderstood? We share highlights from the first-ever national survey of co-buyers.

Written by Pam Hughes, Team CoBuy, Matt Holmes

📊 Looking for the latest? Read CoBuy's 2026 National Report on Co-buying & Co-ownership →

💡 At a glance

• Co-buying is when folks who aren’t married to one another team up to buy and own a home

• CoBuy surveyed 476 U.S.-based co-buyers to listen and learn

• We found that co-buyers are diverse, but they share common motivations and face similar challenges

A co-buyer is an individual or a couple who buys a home with a friend, family member, partner, or another couple. This year, we estimate co-buyers will purchase 25% of all homes sold in the U.S.1

So why are co-buyers still underserved and misunderstood?

Introduction: co-ownership is popular, but difficult

Co-buying and co-ownership aren’t recent phenomena: humans have shared homes throughout recorded history. In fact, the nuclear household didn’t become the dominant household setup in America until the late 1800’s2. Since the 1980s, the proportion of nuclear households across America has declined. Over that same period, we’ve seen an increase in co-buying and co-ownership. In 2020, multi-generational buyers and unmarried couples accounted for 15% and 9% of all home purchases, respectively3.

Times are changing, but the system ain’t. Today, nearly every aspect of buying and owning a home caters to the married couple or the individual. The home-buying process, the real estate industry, and institutions have failed to evolve to address co-buyers and co-ownership. On the front-end, the mortgage application process and underwriting procedures haven’t adapted. On the back end, legal and tax regimes fall short. Co-buyers face challenges at every step: before, during, and after the purchase. The lack of resources and support creates added cost, uncertainty, and risk.

The absence of a framework and structure around co-buying causes friction, or worse—creates a barrier to homeownership and wealth creation. We know because we’ve been there. Our own experience inspired us to start CoBuy back in 2016. In 2021, co-buyers are a huge and underserved segment of the population.

CoBuy Survey Results

You likely know a co-buyer, but they probably never used the term “co-buyer”. When we started CoBuy, Googling co-buy a home returned Japanese manga websites. There’s still a dearth of quality information and resources for co-buyers.

It’s easy to understand why co-buyers struggle. When you don’t know what you don’t know, how do you know which questions to ask? To better understand the needs, wants, and desires of co-buyers today, we conducted a survey of 476 co-buyers planning a purchase within two years.

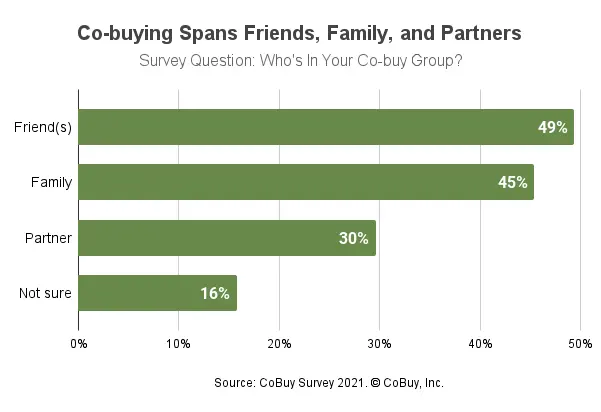

Co-buy groups come in all shapes and sizes

When asked “who do you plan to co-buy a home with?”, half of co-buyers said they plan to purchase with a friend (or friends). Somewhat surprisingly, more respondents reported plans to co-buy with a friend than with family members or their partner.

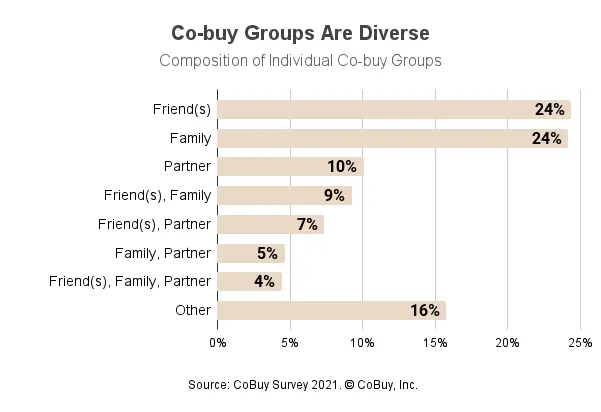

The chart above groups responses by relationship type, but many co-buyers indicated plans to co-buy as a mixed group (e.g. a couple plus a relative). In fact, more co-buyers said they plan to co-buy as a mixed group (31%) than with friends only (24%), family only (24%), or their partner only (10%).

Co-buyer characteristics were as diverse as group composition:

- Groups sizes ranging from 2 to 10+ co-buyers

- First-time homebuyers, veteran homebuyers

- Spectrum of ages (20s through 80s)

- Owner-occupants, non-occupant investors (e.g. parent helping kids)

In most cases, at least one member of the group had plans to reside at the property as an owner-occupant.

The data evolves. Your plan should too.

Assess your group's alignment before you commit.

Get your CoBuy Decision Brief™ →

$250 per group

Financial and social factors drive the decision to co-buy

Why would anyone team up to buy and own a home? Our long-time hypothesis is that social and financial factors are the key drivers. We formed this hypothesis nearly five years ago. Since then, we’ve had thousands of interactions with co-buyers and still this hypothesis remains intact.

It’s time for an update—we got it backwards.

It turns out people care about their money. A lot. But is money really what drives co-buying, and is it more important than the social side of things? Not necessarily. Digging into the open-ended survey data, we found strong support for several other hypotheses:

Co-buyer motivations are dynamic and they’re often inextricably linked.

Example: I want to own a home on an emotive level and for financial reasons.

A motivating factor may consist of both pain-driven elements and pleasure-driven elements.

Example: I want to co-buy because pooling resources to buy a home makes homeownership more affordable. I’m also tired of spending $1,500 a month on rent to fund my landlord’s mortgage.

Many co-buyers are not able to fully articulate their motivations.

Example: I want to co-buy because I already live with my girlfriend and it just seems to make sense.

Other reasons given by respondents included building generational wealth, preparing for retirement, and gaining access to amenities or homes that wouldn’t otherwise be accessible.

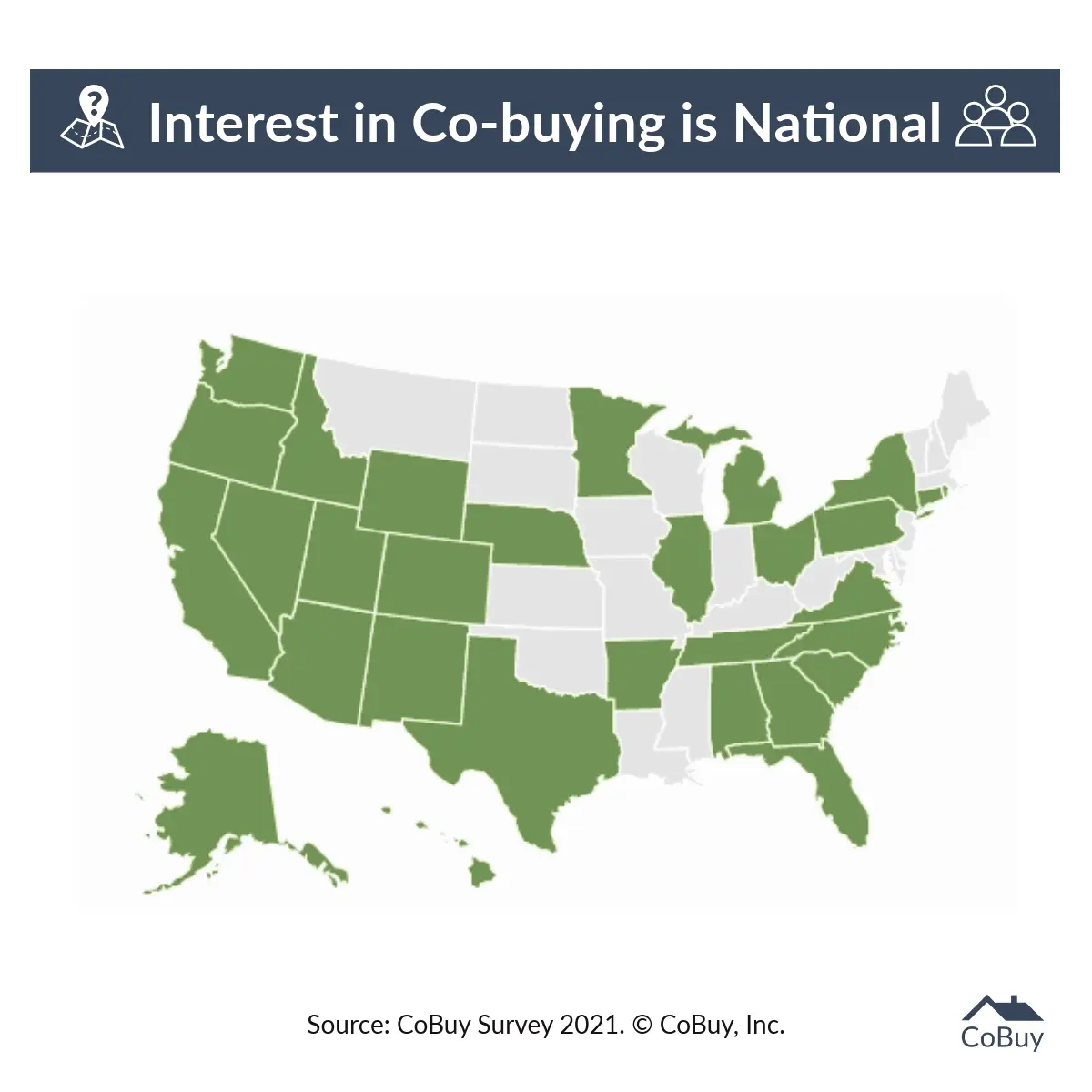

Co-buying is happening across the country

Is co-buying confined to pricey west coast metros? Hardly. Respondents came from 30 states, Puerto Rico, and Guam. Co-buying interest spanned urban cores, suburbs, and rural areas.

No one pattern dominated in terms of geographic migration. As you’d expect, many co-buyers are purchasing in the same region they currently call home. A significant number of co-buyers are mobile:

- Moving outward from urban cores

- Moving from higher-cost metros to lower-cost metros

- Purchasing a second home in another city or state

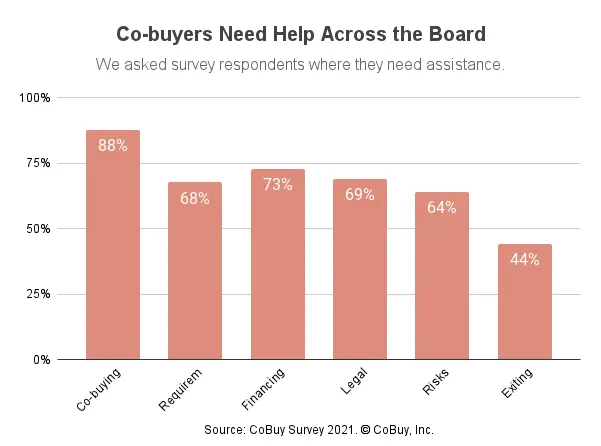

Uncertainty and overwhelm

To hone in on where co-buyers have questions, experience difficulties, or need support, we asked open-ended and closed-ended questions.

In the open-ended section, the most frequently asked question we received was “how does it work?” We grouped all the questions we received into as few discrete categories as possible, ending up with:

- General

- Co-buying Process

- Financing & Eligibility

- Asset/Liability

- Legal & Structuring

- Risks & Protection

- Tax & Accounting

- Co-ownership

- Exit

- Edge Cases

Separately, we asked respondents to identify problem areas from a list of predefined options. The results tell a similar story.

Co-buyers need help

The key takeaway from this survey is that co-buyers desperately need expert guidance.

Anyone who buys a home stakes considerable time, energy, and money. For co-buyers, relationships are also at stake.

Our survey confirms that co-buyers:

- Lack information related to a complex transaction and significant life investment

- Recognize that co-buying involves unique challenges and risks

- Value their own social and financial wellbeing

Taken together this creates a dilemma, and a barrier to attaining the benefits of co-ownership. Ignoring this dilemma is unwise. Likewise, it’s not reasonable to expect a real estate agent or a loan officer to plug the gap. A real estate agent’s job is to sell a house. A loan officer’s job is to sell a loan. While both professionals and functions are important, neither job description includes navigating a joint purchase, creating a framework for co-ownership, and protecting against the risks. It’s not their job.

Keys to success

Co-buying appeals to millions because it improves flexibility, access, and affordability around homeownership. Ironically, our institutions still treat co-buying and co-ownership as non-standard. Rather than supporting folks who choose to co-buy, these institutions add friction. As a result, co-buying is often reduced to a transaction.

We propose a more holistic approach that views co-buying as a journey that includes transacting and culminates in co-ownership. Because co-buying is complicated, it’s helpful to break the journey down into segments. The keys to success are not complicated:

- Quality information

- Planning and structure

- The right professional support

In our experience, co-buyers who incorporate these critical elements into their co-buying journey fare better than those who do not.

ℹ️ References

1 Based on 2018-2020 data sets from NAR, Pew Research, U.S. Census, ATTOM Data, and CoBuy.

2 The Atlantic (2020).

3 Business Insider (2020), NAR (2020).

📊 Survey methodology

CoBuy, Inc. conducted a survey of 476 U.S.-based adults who self-identified as planning to co-buy a home with friends, family members, and/or a partner within 24 months. This survey included closed-ended and open-ended questions. Responses were collected between the fourth quarter of 2020 and the first quarter of 2021. Respondents came from 30 states, Puerto Rico, and Guam. Respondents were not paid. Data has been aggregated and edited for style and clarity.

This blog post was originally published on our old CoBuy blog (https://blog.gocobuy.com) on March 24, 2021. We've brought it over to our new CoBuy blog (https://www.cobuy.io/blog). The content of this post is copyrighted to CoBuy, Inc.

Research informs. Co-ownerOS™ delivers.

Agreements, expenses, exit plans—one place, one platform.

Get your Co-ownerOS™ Annual Pass →

$1,000/year per group · Agreement, expenses, equity, exit planning

How to cite

Preferred citation: "Co-buying a Home in 2021 Report," CoBuy (cobuy.io/blog/cobuying-a-home-2021-report).

Plain-text form: Co-buying a Home in 2021 Report, CoBuy, cobuy.io/blog/cobuying-a-home-2021-report.

Example: “25% of U.S. home purchases involved co-buyers (the CoBuy Co-buying Rate™) in 2021, per CoBuy's 2021 report.”

© 2026 CoBuy, Inc. Citation & reuse. You're welcome to cite these figures and grades for editorial, educational, or personal use with attribution to CoBuy and a clean, followable link to this page: standard hyperlinks only, with no nofollow, noreferrer, or sponsored qualifiers and no redirect wrappers. Commercial use is by license only: republication at scale, resale, syndication, or inclusion in any commercial product, dataset, or AI training corpus requires a license from CoBuy, Inc. Charts and scorecard graphics must keep the embedded source line intact. Licensing: contact.