Buying a House Not Married? How to Protect Yourself

Unmarried couples can co-own homes, but they need to be strategic. Learn how to protect yourself and de-risk your investment.

What we’ll cover:

Why don’t you just get married?

Six short words guaranteed to piss off many folks who haven't tied the knot. But that's what everyone demanded of me daily ten years ago. In two weeks, I broke every rule to adulting: I quit my job, moved to a new city with my partner, started a business, and kicked off my first home search. Friends and family kept asking. I wanted to respond with a prying question about their nighttime activities, but I was sensible back then. The truth is, I didn't want to get married.

But they had a point.

Life is hard for unmarried couples. Marriage is the default marital status in the US in legal matters, finance, insurance, estate planning, healthcare, taxes, government assistance, and property ownership, the main driver of household wealth.

Practically, married couples enjoy legal rights, protections, and benefits denied to unmarried couples. Why?

Can unmarried couples buy a house together?

Yes. There's no law preventing unmarried couples from buying a home together. Under the Fair Housing Act and Equal Credit Opportunity Act, lenders cannot discriminate based on marital status. You can both be on the mortgage, both be on the deed, and both build equity.

What's different is everything that happens after closing. Married couples have a legal framework that governs property rights, asset division, and inheritance. Unmarried couples don't. You have to build that framework yourselves.

Why more unmarried couples are buying homes together

Surely, most households are headed by a married couple, and unmarried couples make up a tiny fraction of the US population. Right?

Negative. The proportion of married couple households is down to just 47%, traditional nuclear households have fallen to 18%, and cohabitating couples are on the rise. Roughly one in ten home purchases each year involve an unmarried couple, and that share is growing at 3.5x the rate of married couple households.

According to the Pew Research Center, 59% of US adults aged 18 to 44 have lived with an unmarried partner at some point. For the first time, one-quarter of 40-year-olds have never been married. So what's up? Most folks want to get married, but they're blocked. Research from the American Survey Center nails it:

- This trend is a reversion to the norm more than a cultural shift

- Starting a family today is expensive

- Young people have little faith in “formative institutions”

In other words, the system is broken.

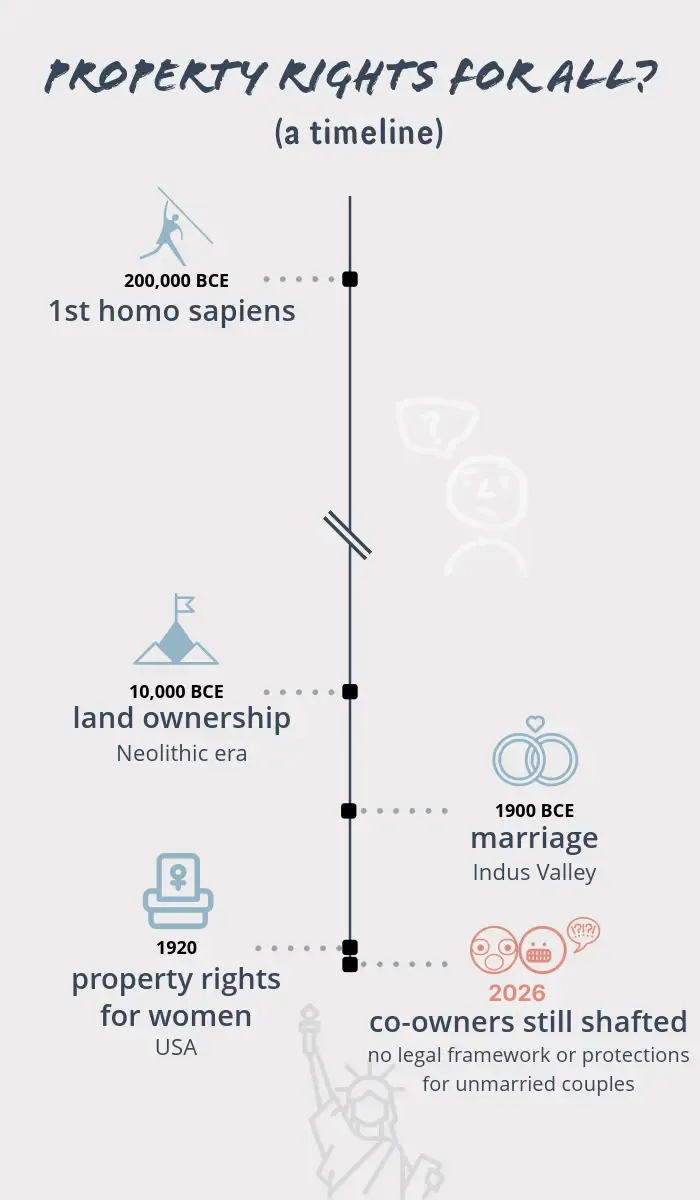

The great irony? Marriage is a relatively recent phenomenon, legal property rights for women are practically brand-spanking-new, and we chose the wrong template for homeownership.

What legal protections do unmarried couples lack?

Unlike married couple homeowners, unmarried couples lack automatic legal rights, protections, and benefits. This impacts every aspect of owning a home and building wealth.

The obvious elephant in the room is the possibility of a breakup. But that's the tip of the iceberg.

Property rights

In most states, married spouses have automatic rights to the marital home. If your name isn't on the deed, you may have zero legal claim to the property, even if you've been making mortgage payments for years. How this plays out depends partly on whether you live in a community property state (like California, Texas, or Washington) or a common law property state (the majority). In community property states, assets acquired during marriage are automatically shared. In common law states, ownership follows the title. For unmarried couples, the distinction matters less because neither framework protects you. Ownership comes down to what's on the deed and what's in writing.

Asset and liability management

Understanding both sides of co-ownership is crucial. Partners need to know who owns what and who owes what. If a mortgage or other liability is in one person's name, they may bear a disproportionate risk. If the property title is in one person's name, the other may not be a legal co-owner. Different types of participation, such as co-owners, co-borrowers, occupants, non-occupant investors, co-signers, and creditors, carry distinct rights, responsibilities, and risks.

Finances

Joint financial accounts can streamline payments, but they can also introduce risk and require oversight. More generally, comingling assets, intentionally or otherwise, can cause trouble and carry tax implications. While most of us may struggle to imagine our partner engaging in nefarious financial activity, a recent study found that 2 in 5 partnered Americans have committed financial infidelity.

Taxes

Unlike married couple homeowners, unmarried couples don't benefit from unlimited gifts between partners or an unlimited deduction for estate tax purposes. Married couples can claim a combined $500,000 capital gains exclusion on a primary residence. Unmarried couples get the individual $250,000 exclusion and can't transfer assets between each other without potential gift tax implications. They also need to work out who will claim eligible tax deductions.

Survivorship and estate planning

If a married spouse dies, property typically transfers to the surviving spouse. For unmarried couples, the deceased partner's share goes through probate and may pass to their parents, siblings, or other heirs unless you've explicitly planned otherwise. Without the legal protections of marriage, estate planning is vital. Co-owners must set up powers of attorney, plan for wealth transfer, and designate beneficiaries.

Healthcare

Unmarried co-owners can face challenges in healthcare decisions and benefits. Without the legal status of marriage, they may lack the right to make medical decisions for each other or to access one another's medical records in emergencies. They may also be ineligible for spousal benefits under Social Security, Medicare, or health insurance policies.

Lack of legal clarity

Some states have limited the rights of unmarried co-owners based on a view that relationships between partners who co-own property are "immoral" or "illicit" by nature. Requirements and treatment of Co-ownership Agreements also vary from one state to another. States like Texas require agreements between parties to be written, while California and Washington take different approaches.

Disputes and breakups

Divorce has an established legal process. Breaking up while co-owning a home has no prescribed sequence. Courts treat it as a property dispute, not a family matter. If you can't agree on what to do with the property, either co-owner can file a partition action to force a court-ordered sale. That's expensive, slow, and adversarial. A Co-ownership Agreement prevents it.

Documentation

Unmarried couples face a much higher bar for record-keeping and accounting than married couples. If a mortgage is in one partner's name, only that partner can claim a deduction for mortgage payments and interest, even if the other partner made financial contributions. Parties should properly document ownership interest in the property.

Common law marriage

Some people assume that living together long enough creates legal rights similar to marriage. In most states, it doesn't. Only a handful of states (Colorado, Iowa, Kansas, Montana, New Hampshire, South Carolina, Texas, Utah, Rhode Island, and the District of Columbia) recognize common law marriage, and each has specific requirements beyond just cohabitation. Don't assume you're protected. A few states also offer domestic partnership or civil union registration, which can provide some property protections similar to marriage.

Social judgment

Despite the growing trend of joint homeownership, social stigma still exists in some places. We've encountered professional service providers in and around residential real estate who don't bother hiding their opposition to unmarried couples cohabitating. Unfortunately, some folks are still operating in the dark ages.

How mortgage qualification works for unmarried couples

Lenders evaluate unmarried co-borrowers the same way they evaluate any co-borrowers: income, credit score, debt-to-income ratio (DTI), and assets. But there are important strategic decisions to make.

One borrower or two?

You can apply for a joint mortgage together or have one person apply alone. Applying together lets you combine incomes, which may qualify you for a larger loan. But lenders use the lower of the two middle credit scores when both people are on the application. If one partner has a 750 and the other has a 620, the lender prices the loan based on 620. That means a higher interest rate and potentially thousands more in interest over the life of the loan.

Credit score thresholds

Most conventional loans require a minimum credit score of 620. FHA loans go as low as 580 with 3.5% down, or 500 with 10% down. If one partner is below these thresholds, leaving them off the mortgage application may seem like the better move. But be careful (see below).

DTI ratio

Lenders typically want your total monthly debt payments (including the new mortgage) to stay below 43% of gross monthly income, though many prefer 36% or lower. If one partner carries significant debt (student loans, car payments, credit cards), their DTI could drag down the joint application even if their income helps.

Be cautious about the "one person on the loan" strategy

In practice, many real estate agents and loan officers steer unmarried couples toward having only one partner apply for the mortgage to get a better rate. That can work, but only if you understand the full picture. Even if just one person is on the loan, the lender's security instrument (deed of trust or mortgage) typically requires everyone on the deed to sign, ceding first lien position to the lender. More importantly, this creates an asset-liability mismatch: one person owns a share of the property but has no legal obligation to the lender, while the other person carries 100% of the debt obligation.

What happens too often: the agent or loan officer steers one partner off the loan AND off the title. Now that person is contributing to the mortgage every month with zero ownership stake. They're a renter who thinks they're an owner. We've seen this happen repeatedly. If you go this route, make sure both partners are on the deed regardless and that a Co-ownership Agreement documents each person's rights and obligations.

How to protect yourself when buying a house with a partner

Romance and ROI can and should coexist. Do tough discussions sound unsexy? Imagine what can go wrong compared to what can go right: building wealth and smooth sailing.

1. Get both names on the deed

If only one person is on the deed, only one person is a legal owner. Full stop. We've seen couples where one partner made the down payment, both made mortgage payments for years, and the non-titled partner had zero legal claim when the relationship ended.

Decide on your title structure:

Tenants in common (TIC). Each person owns a defined share (can be unequal, like 60/40). Shares pass to heirs, not automatically to the other partner. This is the most flexible option for unmarried couples.

Joint tenants with right of survivorship (JTWROS). Equal shares with automatic transfer to the surviving partner on death. No probate required, but ownership must be 50/50.

Living trust. One or both partners can hold title through a revocable living trust. This adds estate planning flexibility, avoids probate, and can specify exactly what happens to the property if either partner dies or becomes incapacitated. More complex to set up, but worth considering if you have significant assets or children from prior relationships.

For most unmarried couples, TIC with a Co-ownership Agreement gives you the most flexibility and protection. Compare TIC vs JTWROS in detail.

2. Create a Co-ownership Agreement

This is the single most important thing you can do. A Co-ownership Agreement is a legally binding document that covers:

- Ownership percentages and how they're determined

- How mortgage payments, taxes, insurance, utilities, and maintenance are split

- What happens if one person wants to sell

- What happens if you break up

- Buyout terms and pricing

- Dispute resolution process

- What happens if one person dies

According to our Co-buying and Co-owning a Home 2025 Report, 94% of US co-buyers need one. Without it, you're relying on verbal agreements that have no legal standing. Get started with the CoBuy Wizard.

Once you have a Co-ownership Agreement, consider recording a Memorandum of Agreement with the county. This is a summary document filed in public records that puts third parties (lenders, title companies, potential buyers) on notice that a Co-ownership Agreement exists. It doesn't disclose the full terms, just the fact that one is in place. This is a layer of protection most people don't know about.

3. Decide how to split costs and contributions

Not all contributions are equal, and that's fine. What matters is that you document them.

Down payment. If one person puts in $80,000 and the other puts in $20,000, ownership percentages should reflect that, or you should document the arrangement (like a loan between partners) in your Co-ownership Agreement.

Monthly expenses. Mortgage, taxes, insurance, HOA, utilities, maintenance. Agree on the split, automate payments, and track everything. Here's how to split ownership fairly.

Non-financial contributions. Renovations, domestic work, property management. Consider assigning monetary value to these and documenting them. In a breakup, proof of contributions becomes critical.

4. Plan for the worst cases

These aren't fun conversations. They're necessary.

If you break up. Who gets the house? At what price? How long does the departing partner have to move out? Can one person force a sale? Without a Co-ownership Agreement, either party can file a partition action, a legal proceeding that forces a court-ordered sale of the property. Partition actions are expensive, time-consuming, and adversarial. They're the nuclear option, and your Co-ownership Agreement is what prevents them. Document buyout terms, right of first refusal, appraisal methods, and a timeline upfront. The time to negotiate is when you're in love, not when you're hiring separate lawyers.

If one person dies. Without survivorship rights or a will, your partner's share goes to their legal heirs, not to you. Both partners need updated wills, healthcare proxies, HIPAA releases, and durable powers of attorney. Also consider a life insurance policy naming your partner as beneficiary. Life insurance proceeds bypass probate entirely and can provide immediate funds for the surviving partner to cover the mortgage, buy out heirs, or manage the transition.

If one person loses their job. How long can the other person cover the full mortgage? What triggers a conversation about selling? At what point does it become a financial emergency?

If one person wants to sell and the other doesn't. This is the most common co-ownership dispute. Your Co-ownership Agreement should specify a resolution process: right of first refusal, independent appraisal, mediation, and a timeline.

5. Keep meticulous records

The IRS doesn't care about your relationship status. They care about documentation. If a mortgage is in one person's name, only that person can claim the mortgage interest deduction, even if both partners contribute to payments.

Track every payment, every contribution, every agreement. Keep records of who paid what, when, and why. This protects you in a breakup, an audit, a dispute, and at tax time.

6. Get the right help

Don't wing this, and don't rely on your real estate agent or loan officer for guidance on ownership structure, agreements, or legal protections. They're not qualified for that. For most unmarried couples, the core challenge isn't legal complexity. It's alignment: getting on the same page about finances, ownership, responsibilities, and what happens if things change. That's a planning and decision-making problem, not a contract-drafting problem.

A real estate attorney is one option. But the all-in cost often runs $10,000 to $15,000 or more when you factor in hourly rates ($300 to $600+ per hour), multiple sessions with multiple parties, and revisions. Most attorneys don't specialize in co-ownership and produce a static document from a template library. It doesn't help you manage expenses, track equity, or navigate changes over time.

CoBuy was built for this. The CoBuy Wizard walks you and your partner through the alignment process and produces a CoBuy Decision Brief™ covering finances, ownership structure, and key decisions. Co-ownerOS™ goes further: agreement generation, expense management, equity tracking, and exit planning, all built specifically for co-owners. For complex situations involving trusts, blended families, or significant assets, an attorney may be worth consulting in addition. But for the vast majority of unmarried couples buying together, the right tool matters more than the right lawyer.

What 1,600+ co-buyers told us about co-ownership

We've worked with many unmarried couples over the last nine years. It's not all about the breakup or disaster scenarios.

1. Unmarried couples want help with day-to-day co-ownership management.

We've surveyed over 1,600 US-based co-buyers and co-owners, with unwed partners accounting for 29% of all respondents. When asked where they most need help managing shared homeownership:

- Co-ownership Agreement (94%)

- Finances, expenses, payments (69%)

- Documentation and records (66%)

- Roles, rights, responsibilities (66%)

- Legal (66%)

- Exit strategy (63%)

- Tax and accounting (60%)

- Risk protection (59%)

- Admin (49%)

The pattern is clear: day-to-day management dominates. Nearly everyone needs a Co-ownership Agreement. The operational stuff (finances, documentation, roles) outranks the things people worry about most (legal, exit strategy).

💡Example

Imagine that each co-owner spends 10 minutes daily managing, troubleshooting, and dedicating time to co-ownership.

10 minutes x 365 days x 2 co-owners = 122 hours per year

If you make $75k a year, that’s nearly $5k a year in earnings equivalent. This figure excludes lost time, opportunity cost, stress, and compounding interest.

2. Every situation is different.

In our first Co-buying a Home Report, we surveyed 476 US-based co-buyers. Our sample set showed a higher incidence of unmarried couples co-buying together with at least one other friend or family member than unmarried couples co-buying as a pair. These are two very different dynamics. It's like playing Catan against your honey bunny versus playing a full table.

These responses track with our experience. Different group sizes and compositions affect dynamics, which impacts where folks need help.

3. For many couples, this isn’t their first rodeo.

Some have previously owned a home, been through a divorce, and have kids from prior relationships. These folks are generally more risk aware. They've been through decoupling before and are serious about protecting themselves, their children, and their partner.

FAQs

Do we need a Co-ownership Agreement if we trust each other?

Yes. The IRS, probate courts, your lender, and insurers don't care whether you trust each other. Your relationship can be great, and a lack of documentation can still create serious problems. Treat documentation like your passport on a trip to Russia. Don't get caught without it.

What if the deed or mortgage is only in one person's name?

A co-owner who isn't on Title is probably not a co-owner. We've seen many instances of unmarried couples relying on their real estate agent, loan officer, and title company at the time of purchase, only to learn later that one of them is effectively a renter. Not documented? It didn't happen. Be mindful that any changes to participation on the deed or modifications to Title could trigger a due-on-sale clause and a taxable event.

Does common law marriage give us property rights?

In most states, no. Only about ten states plus Washington, D.C. recognize common law marriage, and each has specific requirements beyond simply living together. Length of cohabitation alone doesn't create a common law marriage anywhere. If you're in a state that does recognize it (Colorado, Iowa, Kansas, Montana, New Hampshire, South Carolina, Texas, Utah, Rhode Island, or D.C.), consult a qualified professional to determine whether you qualify. Don't assume.

What is a partition action?

A partition action is a legal proceeding where one co-owner asks the court to force the division or sale of jointly owned property. If you and your partner can't agree on what to do with the house after a breakup, either of you can file one. The court typically orders the property sold and the proceeds split according to ownership shares. It's expensive (legal fees on both sides), slow (months to over a year), and public. A well-drafted Co-ownership Agreement with buyout terms and dispute resolution provisions is designed to prevent this.

How do we handle unequal financial contributions?

Make a list of all recurring expenses (mortgage payments, utilities, taxes, insurance, etc.) and non-recurring expenses, agree on how you'll split these, and align on the mechanics of payment. Document everything in your Co-ownership Agreement and update it as needed. You should also provision for unexpected expenses such as maintenance, repairs, and emergencies by creating and funding a Reserve Account.

What about non-financial contributions?

It's common for co-owners to make non-financial contributions of time, work, or skills. Get on the same page about what each party will bring and set clear expectations. You may consider assigning a monetary value to non-financial contributions such as domestic work, renovations, or caretaking. Be sure to document everything in your Co-ownership Agreement and keep it up-to-date. In certain situations like a breakup, job loss, audit, or death, proof of individual contributions prove invaluable.

What's the difference between a Co-ownership Agreement and a cohabitation agreement?

Co-ownership Agreements are more specific in scope and offer greater legal clarity. Cohabitation agreements are not unique to the co-ownership of real property and are often broader in scope. The two aren't mutually exclusive, though creating and maintaining both may be redundant. If you co-own a home, you need a Co-ownership Agreement.

Why do we need to track expenses?

To protect your relationship, home, and largest asset. And because the IRS says so.

Do we need a real estate attorney?

Not necessarily. An attorney can be helpful for complex situations (trusts, blended families, significant asset disparity, unusual state laws). But for most unmarried couples, the real need is a structured process for aligning on ownership, finances, and contingencies, plus an agreement that reflects those decisions. That's what CoBuy is designed to do. If you do work with an attorney, make sure they specialize in real estate or co-ownership, not just general practice.

Everyone should have access to homeownership, regardless of background, orientation, or living arrangement. The system is broken and needs an overhaul. We're fixing it.

This guide is for informational purposes only and does not constitute legal, tax, or financial advice. Consult qualified professionals for guidance specific to your situation.

Check out our other posts:

Ultimate guide to shared homeownership

The 3 stages of shared homeownership