Home Co-ownership: What It Is and How It Works

Home co-ownership is when 2+ people who aren't married share ownership of a home. Learn how it works, the risks, how to hold title, and how to protect yourself.

Home co-ownership is when two or more people who are not married to one another share ownership interest in a home. Over 64 million Americans co-own a home with someone who isn't their spouse, and 31.5% of US home sales now involve co-buyers. Whether you're buying with a friend, a relative, an unmarried partner, or a mix, co-ownership can make homeownership accessible when going solo isn't an option.

But co-owning a home is more complex than buying one on your own. You're managing shared finances, legal structures, decision-making, and risk across years or decades. This guide covers how co-ownership works, the most common structures, financing, risks, and what you need to do to protect yourself.

Featured by

What we'll cover:

- What is home co-ownership?

- Who co-owns homes?

- Quiz: What's your co-buy group type?

- How co-buying a home works

- Types of co-ownership: TIC vs. Joint Tenancy

- The co-ownership lifecycle

- Benefits of co-owning a home

- Risks of co-owning a home

- The Co-ownership Agreement

- Finances, expenses, and payments

- Decision-making and dispute resolution

- Exit strategies

- How to protect yourself as a co-owner

- FAQ

What is home co-ownership?

Home co-ownership is when two or more people who are not married to one another share ownership interest in a home. Other common terms include shared homeownership and joint homeownership.

You can co-own a home with a friend, relative, partner, or a combination. Even married couples co-own homes. CoBuy's Co-buying & Co-owning a Home 2026 Report found that 16% of all co-ownership arrangements involve a married couple plus at least one other co-owner.

Co-ownership isn't new, but it's growing fast. With median home prices well above $400,000 and mortgage rates elevated, more people are pooling resources to get into homeownership. According to CoBuy's 2025 survey of 1,637 co-owners, the top motivations are affordability, building wealth together, and accessing neighborhoods that would be out of reach individually.

CoBuy has helped thousands of co-buyers and co-owners across $61M+ in transactions since 2016. With 61 years of combined experience across real estate, finance, insurance, and construction, we've spent over 51,500 hours working directly with co-ownership groups.

📊 Co-habitation in numbers

• Relatives: nearly 20% of the US population lives in a multi-generational household

• Partners: unmarried couples make up about 8% of all US households

• Friends: 4% of all home buyers are friends co-buying together

Nuclear households now account for less than half of the national total, with over 18 million jointly-owned homes comprising 61 million co-owners in the US. Unfortunately, the systems that facilitate homeownership, including financial, legal, tax, and insurance, were designed for married couples or individuals buying solo. Co-owners face more complexity, more costs, more uncertainty, and more risk across the entire homeownership lifecycle.

ℹ️ Co-owners don’t enjoy the same legal and tax protections as married couples if someone dies, becomes incapacitated, or has disagreements.

Who co-owns homes?

Friends. Buying a house with friends is increasingly common, especially among millennials and Gen Z buyers who've been priced out of solo ownership. Friends typically split costs equally and hold title as Tenants in Common.

Family members. Buying a home with family includes adult children buying with parents, siblings pooling resources, or multi-generational households. Family co-ownership often involves unequal contributions, which makes the title and equity structure more complex.

Unmarried partners. Unmarried couples are one of the fastest-growing co-buying segments. Without the legal protections that marriage provides (community property laws, automatic survivorship, spousal rights), unmarried partners need to be especially deliberate about structuring ownership and creating a Co-ownership Agreement.

Mixed groups. A married couple buying with a friend or parent. Two couples buying together. Three siblings and a cousin. These arrangements are more common than you'd think: CoBuy's 2025 Report found that 15% of co-ownership groups include a married couple plus at least one additional co-owner.

Each relationship type brings different dynamics, risks, and legal considerations. The common thread: all of them benefit from a structured approach to alignment, documentation, and ongoing management.

Interactive quiz

What type of co-ownership group are you?

4 questions. Under a minute. See your group profile, top risks, and what to read next.

How co-buying a home works

The process of co-buying follows the same basic steps as any home purchase, with a few critical additions.

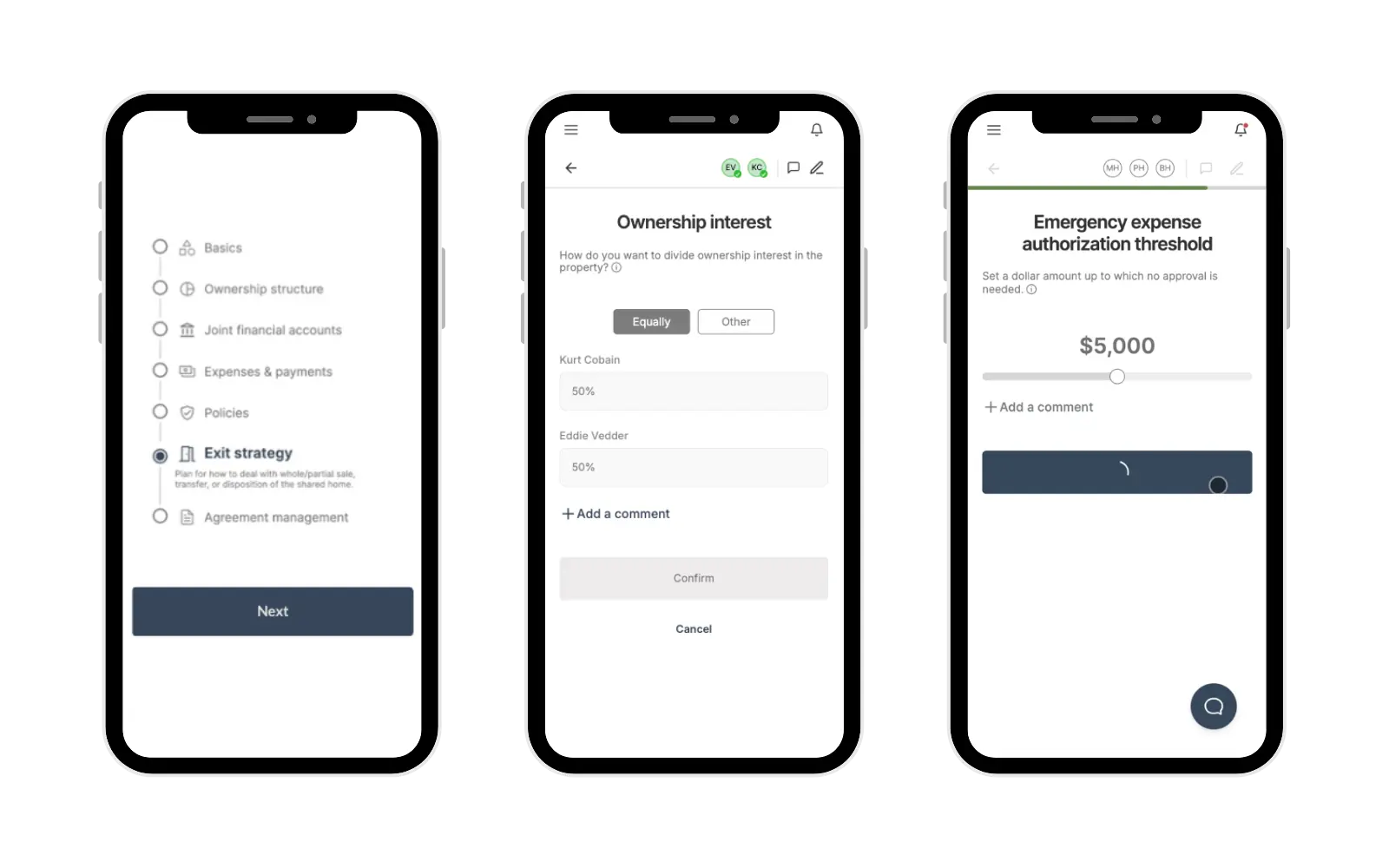

- Get aligned before you start shopping. This is where most co-buyers skip ahead and pay for it later. Before you look at a single listing, your group needs to discuss budget, ownership split, contribution ratios, living arrangements, and what happens if someone wants out. CoBuy's Wizard guides groups through this alignment process and produces a CoBuy Decision Brief™ covering all the key decision points.

- Get pre-approved for a mortgage. Co-buyers apply for a mortgage together. No special loan product is required. Lenders evaluate the combined income, assets, and debts of all co-borrowers, but here's the catch: the interest rate is based on the lowest credit score among all applicants. A co-buyer with a 620 credit score will drag the rate for the entire group, even if everyone else is above 780.

All co-borrowers are jointly and severally liable for the full mortgage amount. If one person stops paying, the others must cover it or face foreclosure and credit damage

Use CoBuy's budget calculator to estimate what your group can afford based on combined income and expenses.

- Choose how to hold title. Before closing, your group must decide whether to hold title as Tenants in Common (TIC) or Joint Tenants with Right of Survivorship (JTWROS). This decision affects ownership shares, survivorship rights, transferability, and what happens if a co-owner dies. More on this below.

- Create a Co-ownership Agreement. This is the single most important document in any co-ownership arrangement. It covers ownership structure, financial contributions, decision-making, dispute resolution, and exit procedures. Do this before or at closing. See the Co-ownership Agreement section below.

- Close and take ownership. At closing, all co-buyers sign the mortgage documents and the deed is recorded with the title structure your group selected. From this point forward, you're co-owners.

- Manage co-ownership actively. This is where most groups drop the ball. Co-ownership doesn't run itself. Ongoing management includes tracking expenses, maintaining documentation, making joint decisions, and updating your Co-ownership Agreement as circumstances change. Co-ownerOS™ is built specifically for this.

Types of co-ownership: TIC vs. Joint Tenancy

How you hold title determines your legal rights, what happens when someone dies, and how flexible your arrangement is. The two most common structures for co-owners are Tenants in Common (TIC) and Joint Tenants with Right of Survivorship (JTWROS).

| Tenants in Common (TIC) | Joint Tenancy (JTWROS) | |

|---|---|---|

| Ownership shares | Equal or unequal (e.g., 60/40, 70/30) | Equal and undivided only |

| Right of survivorship | No. Share passes via will or intestate succession. | Yes. Share passes automatically to surviving co-owners. |

| Probate on death | Yes, unless other estate planning is in place. | No. Bypasses probate. |

| Can sell/transfer share independently | Yes (may be restricted by Co-ownership Agreement). | Yes, but doing so severs the joint tenancy. |

| Default in most states | Yes (if deed doesn't specify). | No. Must be explicitly stated in the deed. |

| Best for | Friends, family with unequal contributions, investor + occupant combos. | Married or committed couples, close family who want automatic transfer. |

Tenants in Common allows co-owners to have equal or unequal ownership interests as a percentage. Upon the death of a co-owner, their ownership interest passes to the beneficiary specified in their will. TIC is the default title structure in most states if the deed doesn't specify otherwise.

Joint Tenants with Right of Survivorship creates equal and undivided ownership interests. If a co-owner dies, their ownership interest transfers automatically to the surviving co-owner(s), bypassing probate. JTWROS requires the "Four Unities" (time, title, interest, and possession) and must be explicitly stated in the deed.

Other structures include LLCs (useful in some scenarios but introduces complexity and costs) and trusts (relevant for estate planning situations).

For a deep dive on how to choose, see our full guide: JTWROS vs Tenants in Common: How Co-Buyers Hold Title. You can also take the interactive quiz to see which structure may fit your group.

💡 Pro tip

The format of Title is established when the property is first transferred to co-owners. The deed that transfers the property will specify the type of Title being conveyed. Title can be changed later, but it may require a new deed, lender involvement, and/or recording costs.

The co-ownership lifecycle

Most resources treat co-buying as a one-time transaction. It isn't. Every co-ownership arrangement moves through three stages:

1. Co-buying. The pre-purchase phase: alignment, mortgage qualification, house hunting, title selection, creating your Co-ownership Agreement, and closing. This is where you set the foundation. Mistakes here compound for years.

2. Co-owning. The ownership phase: managing joint finances, tracking expenses, maintaining the property, making decisions together, handling life changes, and keeping documentation current. This stage can last years or decades, and it's where most problems emerge.

3. Exit. 100% of co-ownership arrangements eventually end through sale, buyout, transfer, or death. Planning for exit before you buy is essential. See Exit Strategies below.

Success means maximizing benefits and minimizing costs across all three stages. CoBuy's products map to this lifecycle: the CoBuy Wizard handles alignment in the co-buying phase, and Co-ownerOS™ provides governance and operations tools for the co-owning and exit phases.

For the full lifecycle framework, see: How to Co-Own a Home: Buy, Own, and Exit Together.

Benefits of co-owning a home

Affordability. Splitting the down payment, closing costs, and monthly mortgage payments makes homeownership possible for people who can't qualify or afford a home on their own. Two incomes on a mortgage application typically qualify for a larger loan amount.

Access to better homes and neighborhoods. Pooled buying power means your group can afford properties in neighborhoods, school districts, or markets that would be out of reach individually.

Shared ongoing costs. Property taxes, homeowners insurance, maintenance, repairs, and utilities split across co-owners reduce the per-person burden. Use CoBuy's budget calculator to model the numbers for your group.

Equity building. Every mortgage payment builds equity. Co-owners share in the property's appreciation over time, creating a wealth-building path that renting doesn't offer.

Flexibility in living arrangements. Co-ownership works for people who live together and for those who don't. Non-occupant co-owners (investors, parents helping adult children) are common, especially in family co-ownership arrangements.

For a broader look at cost factors, see: Hidden Costs of Co-Owning a Home.

Risks of co-owning a home

Co-ownership concentrates your largest asset, your largest liability, and (often) your residence into a single arrangement with other people. The stakes are high.

Use CoBuy's co-ownership risk calculator to assess the specific risks for your group's situation.

Each risk below includes a real-world scenario based on patterns we've seen across thousands of co-ownership groups.

Sunk time and energy

Triggers: Conflict between co-owners, inadequate planning, poor documentation.

Example: Four family members co-own a home in which two are occupants and two are non-occupant investors. A difference in opinion emerges as to whether a leak in the roof constitutes a necessary repair that requires professional work or can be addressed DIY. A three-month argument ensues, during which deadlock prevents any progress. Meanwhile, water damage continues until a total roof replacement is required at $8,000.

Surprise expenses

Triggers: Breakup or divorce among co-owners, death of a co-owner, inadequate planning, missed or late payments, poor documentation.

Example: A group of friends co-owns a home. Roles and responsibilities are left to chance. A communication breakdown results in a missed homeowner's insurance payment, which causes a lapse in coverage just before a burglar breaks in and steals $18,000 worth of electronics. When coverage is resumed, the insurance provider raises the premium by 25%.

Financial loss

Triggers: Death of a co-owner, inadequate planning, job loss, missed or late payments, unauthorized borrowing against the property.

Example: An uncle and adult niece co-own a home. Life events cause the pair to sell sooner than expected when the uncle discovers the niece has tapped equity in the home to purchase a car. The uncle is forced to come out of pocket to cover $12,000 in outstanding debt plus selling costs.

Credit impairment

Triggers: Missed or late payments, unauthorized borrowing against the property.

Example: Two adult parents co-buy a home with their adult son. All parties are co-borrowers on the mortgage. The son fails to make mortgage payments for 60 days. When the parents apply for a car loan the following week, they learn their credit scores have dropped 125 points.

Foreclosure

Triggers: Missed or late payments, unauthorized borrowing against the property.

Example: Three best friends work at the same company and co-own a primary residence. All three are laid off in the same week when the economy enters a recession. Failure to repay the mortgage for four months results in the lender initiating a foreclosure suit. Foreclosure affects every co-borrower's credit for 7+ years.

Litigation

Triggers: Breakup or divorce, conflict between co-owners, death of a co-owner, poor documentation.

Example: Two couples co-own a home at which they alternate occupancy throughout the year. Usage rights have been loosely agreed upon without ever being recorded. An argument over rights to the property during summer months spirals out of control and kicks off an 18-month legal battle.

Forced sale

Triggers: Breakup or divorce, conflict between co-owners, death of a co-owner, missed or late payments.

Example: Following the death of a co-owner, their named beneficiary inherits ownership interest in the home. The succeeding beneficiary is unknown to the surviving co-owners and files a partition action, resulting in a forced sale and a $75,000 bill. Partition actions typically cost $25,000 to $100,000+ in legal fees and take 6 to 18 months.

Probate

Triggers: Death of a co-owner, inadequate planning, poor documentation.

Example: An unmarried couple co-owns a home, holds title as Tenants in Common, and both are co-borrowers on a mortgage. Neither co-owner has a will, nor has the couple created a Co-ownership Agreement. After the untimely passing of one co-owner, a 9-month-long probate process begins. The surviving co-owner is on the hook for the full mortgage and cannot sell the property.

Damaged relationships

Triggers: Conflict between co-owners, inadequate planning, missed payments, poor documentation.

Example: Two single friends co-own a primary residence with equal ownership interest. One co-owner begins a long-term relationship, and their new partner transitions into a full-time roommate despite protests from the other co-owner. Resentment grows, and the friendship never recovers.

For more real-world examples, see our guide to common co-ownership mistakes and co-ownership flashpoints to avoid.

The Co-ownership Agreement

A Co-ownership Agreement is the single most important document in any co-ownership arrangement. It's a written contract between co-owners that covers:

- Ownership structure and equity split

- Financial contributions (down payment, mortgage, ongoing expenses)

- Decision-making rules

- What happens if someone can't pay

- Dispute resolution (mediation, arbitration)

- Exit procedures (buyout, sale, transfer)

- What happens if someone dies, gets divorced, or becomes incapacitated

According to CoBuy's 2025 survey, 94% of co-buyers who aren't married need a Co-ownership Agreement, yet most skip it or use a generic template.

As the first company specialized in home co-ownership and the builders of the first co-buying and co-ownership platforms, we've seen what works and what doesn't across thousands of groups.

What about hiring an attorney? An attorney-drafted Co-ownership Agreement plus a Memorandum of Agreement (MOA) for recording typically costs $10,000 to $15,000 or more. That's out of reach for most co-buying groups, which is exactly why most people don't get one. The alternative isn't to skip it entirely. It's to use a structured process that produces a living, updateable agreement without the five-figure price tag.

CoBuy's approach: the CoBuy Wizard guides your group through alignment on all key decision points and produces a CoBuy Decision Brief™ ($250/group). Co-ownerOS™ then provides ongoing tools to manage and update your agreement as circumstances change.

For a detailed breakdown of what to include and why, see: Co-ownership Agreement: What to Include and Why.

Finances, expenses, and payments

Staying on top of all cash flows is critical. Most expenses fall into two categories:

Recurring expenses that come due at regular intervals: mortgage, homeowners insurance, private mortgage insurance (PMI), property taxes, HOA/condo fees, utilities, and home warranties.

Non-recurring expenses: maintenance, repairs, incidentals, and emergencies.

Here's how to handle them:

Map out all cash outflows. List every expense category and the expected amount. Use CoBuy's budget calculator to model your group's numbers.

Agree on how to divide expenses. Splits don't have to be equal, but they must be explicit. Some groups split proportionally by ownership share. Others split equally regardless of equity percentage. What matters is that everyone understands and agrees to the terms.

Define payment mechanics. Recurring payments come due at different intervals, may be fixed or variable, and need to originate from a single source (the mortgage servicer doesn't accept two partial payments). Decide who pays what, when, and through which account.

Track everything. Hunting for crumpled receipts at tax time or during a dispute is a nightmare. Build a system from day one. Co-ownerOS™ includes expense tracking and documentation tools designed for co-owners.

Record it in your Co-ownership Agreement. Writing it down makes it official and provides a reference when questions arise. As circumstances change, update the agreement.

For more on the financial side, see: How to Split Ownership of a House.

Decision-making and dispute resolution

In dealing with thousands of co-buyers and co-owners, we've observed a clear pattern: a structured approach to joint decision-making delivers the best results. Conversely, things don't end well without an intentional approach to building and maintaining consensus.

Four main drivers of effective joint decision-making:

- Communication. Regular check-ins. Don't wait for problems to surface.

- Transparency. Financial transparency is essential. No surprises about income changes, debt, or spending.

- Coordination. Who handles what? Clear roles and responsibilities prevent things from falling through the cracks.

- Cooperation. Co-ownership requires compromise. Not every decision will go your way.

Dispute resolution. Prevention is the best approach, but disagreements happen. Your Co-ownership Agreement should include:

- Mediation first. A neutral third party helps co-owners reach agreement. Lower cost, lower stakes.

- Arbitration as backup. A binding decision from an arbitrator. Faster and cheaper than court.

- Litigation as last resort. Most real estate attorneys advise against it. Legal battles over co-owned property can exceed the equity you've built and take 12 to 18 months.

See how aligned your group really is

Budget, ownership split, exit plan: surfaced before they become problems.

Get your CoBuy Decision Brief™ →

$250 per group

Exit strategies: what happens when someone wants out

100% of co-ownership arrangements eventually end. Planning for exit before you buy is not pessimistic. It's essential.

Common exit scenarios:

Buyout. The remaining co-owner(s) buy out the departing co-owner's share. This usually involves a home appraisal to determine fair market value and a cash-out refinance to fund the buyout. If interest rates have risen since the original purchase, refinancing may not make financial sense.

Sale. All co-owners agree to sell the property and split the net proceeds according to the equity structure in your Co-ownership Agreement.

Transfer. A co-owner transfers their interest to another person (a new co-owner, family member, or trust). This may trigger a due-on-sale clause in the mortgage and could be a taxable event.

Partition action. If co-owners can't agree on an exit, any co-owner can file a partition action to force the sale of the property through the courts. This is the most expensive and destructive exit: $25,000 to $100,000+ in legal fees, 6 to 18 months, and often results in a below-market sale price.

The best defense against a bad exit is a detailed exit strategy documented in your Co-ownership Agreement before you buy. Include buyout triggers, valuation methods, timelines, and right-of-first-refusal provisions.

How to protect yourself as a co-owner

Create a Co-ownership Agreement before or at closing. This is non-negotiable. See the Co-ownership Agreement section above and our detailed guide.

Choose the right title structure. TIC vs. JTWROS has real implications for your rights, your estate, and your flexibility. See Types of Co-ownership above.

Maintain documentation. Get things in writing and keep all related files, records, and receipts up-to-date. Not documented? Didn't happen. For more on what to keep and why: Co-Ownership Documents: What to Keep and Why.

Get proper insurance. All co-owners should be covered by homeowners insurance. If the property is financed, the mortgage lender will require it. Make sure all co-owners are named on the policy.

Plan for death and incapacity. Each co-owner should have a will that accounts for their ownership interest. If you hold title as TIC, your share passes through your estate, so a will is especially important. Consider life insurance policies that would allow surviving co-owners to buy out a deceased co-owner's share. Estate planning is one area where consulting an attorney is worth the cost.

Use tools built for co-owners. CoBuy's Co-ownerOS provides governance, document management, expense tracking, and agreement management tools designed specifically for co-ownership groups. CoBuy's course covers the fundamentals in more depth.

Assess your risks. Use CoBuy's co-ownership risk calculator to identify the specific risk factors for your group.

Frequently asked questions about home co-ownership

Do you need a special mortgage to co-buy a home?

No. Co-buyers apply for a standard mortgage together. Lenders evaluate the combined income, assets, and debts of all co-borrowers. The main difference: the interest rate is based on the lowest credit score among all applicants, and every co-borrower is fully liable for the entire loan amount.

What happens if one co-owner can't make their mortgage payment?

The other co-owners must cover it. Missing payments affects every co-borrower's credit score and can lead to foreclosure. Your Co-ownership Agreement should address this scenario explicitly, including grace periods, notification requirements, and consequences.

Can you buy a house with a friend?

Yes. Buying a house with friends is increasingly common, especially as housing costs make solo ownership difficult. Friends typically hold title as Tenants in Common and create a Co-ownership Agreement that covers financial contributions, living arrangements, and exit procedures.

Can you buy a house with a family member?

Yes. Buying a house with family members is one of the most common co-ownership arrangements. It often involves unequal contributions (a parent helping an adult child, for example), which makes the equity structure and Co-ownership Agreement especially important.

How do you split ownership of a co-owned home?

Ownership can be split equally or unequally based on financial contributions, occupancy, or other factors your group agrees on. If you hold title as Joint Tenants, ownership must be equal. Tenants in Common allows unequal shares. For a full breakdown: How to Split Ownership of a House: 50/50, 60/40, 70/30.

What is a partition action?

A partition action is a lawsuit where one co-owner forces the sale or division of a co-owned property. Partition actions are expensive ($25,000 to $100,000+ in legal fees), slow (6 to 18 months), and often result in below-market sale prices. A well-drafted Co-ownership Agreement with buyout triggers and mediation clauses is the best defense.

Should co-owners form an LLC?

In most cases, an LLC is not necessary for co-owning a primary residence. LLCs add cost and complexity, may prevent you from deducting property taxes and mortgage interest on personal taxes, and most residential lenders won't finance an LLC-held property. LLCs can make sense for investment properties or rental arrangements, but consult a CPA and attorney first.

What happens if a co-owner dies?

It depends on how you hold title. With JTWROS, the deceased's share passes automatically to surviving co-owners, bypassing probate. With TIC, the deceased's share passes through their estate (via will or intestate succession), which typically involves probate. In either case, your Co-ownership Agreement and estate planning documents should address this scenario. Consider life insurance to fund a potential buyout.

Already co-own a home?

Co-ownerOS helps you manage finances, decisions, and documents together.

Get your Co-ownerOS™ Annual Pass →

$1,000/year per group · Agreement, expenses, equity, exit planning

⚡ Key takeaways

- Approach co-ownership with a business mindset: shared investment, shared risk, shared responsibility.

- Get aligned on budget, ownership split, and exit strategy before you start shopping. The CoBuy Wizard can help.

- Choose the right title structure (TIC or JTWROS) based on your group's contributions, goals, and risk tolerance.

- Create a Co-ownership Agreement before or at closing. This is not optional.

- Plan for exit before you buy. 100% of co-ownership arrangements end eventually.

- Manage co-ownership actively with proper documentation, financial tracking, and regular communication.

- Use Co-ownerOS™ for ongoing governance and CoBuy's free tools to assess your risk profile and budget.

Check out our other posts:

The $350k disaster most co-owners create