How to Split Ownership of a House: 50/50, 60/40, 70/30

Learn how to split ownership interest in a co-owned home with friends, family, or your partner, including factors to consider and how to avoid common pitfalls.

Overview

Whether you decide to co-own a home with your honey, buddy, or grandma, you’ll need to decide how to split ownership. If discussing this feels awkward, you’re not alone. Shared homeownership is a big commitment. Getting on the same page requires clear communication and open and transparent dialogue between co-owners. Not only is this a critical step in the planning process — it helps instill confidence, protect your home, and safeguard your investment.

Some co-owners choose to split ownership interest equally among themselves. Others prefer to divide ownership interest unequally based on factors such as individual contributions or rights to the property. As with many decisions in joint homeownership, there’s no one-size-fits-all solution. What works for an unmarried couple may not suit another unmarried couple, let alone an intergenerational household.

In this post, we’ll explore the factors that drive this decision. We’ll also highlight issues for consideration and share pro tips based on our experience working with hundreds of co-buyers and co-owners.

Which factors impact individual ownership percentages?

Ultimately, it’s up to you and your co-owner(s) to decide how you split ownership interest. Every situation is different, but there are standard points of reference to guide decision making.

Uneven splits are common when two generations buy together, one side brings equity, the other carries the loan. If that is your situation and the challenge is the home itself, start with the compound.

Objective Factors

Participation

It’s essential to establish who will be involved and in what capacity. This sounds simple, but we’ve seen many instances of co-ownership where participation wasn’t clear. At CoBuy, we solve this by helping folks explicitly define:

- List of all participants (involved in any capacity)

- Relationships between all participants

- Participants who will occupy the property

- Participants who will not occupy the property

- Participants on the mortgage (“co-borrowers”)

- Participants on Title (“co-owners”)

Buyer groups of all sizes should complete this exercise.

Financial contributions

Co-owners should work out individual financial contributions, both upfront and on an ongoing basis.

Examples of upfront costs:

- Down payment

- Closing costs

- Pre-paid items (such as insurance, taxes, etc.)

Examples of recurring expenses:

- Monthly mortgage payments

- Insurance

- Taxes

- HOA or condo association dues

- Utilities

This list is not exhaustive. Other expenses and costs can be expected, such as maintenance, repairs, and improvements.

📝 Note

Co-owners can contribute different amounts towards the upfront costs and still choose to divide ownership interest in the property equally.

Non-financial contributions

Participants may bring something to the table other than money. Non-financial contributions can include:

- Specialized skillsets or efforts to improve the property

- Performance of household duties

- Management of the property

- Care-taking of children or elders

You may decide to recognize non-financial contributions or even assign a monetary value.

Usage rights

If your co-ownership plan involves assigning specific spaces or rights, you may choose to reflect this in how you split ownership. Examples include exclusive access to a disproportionately sized bedroom, an alternate dwelling unit (ADU), or an outdoor area.

Subjective Factors

Fairness

Co-owners often seek ownership stakes that are “fair.” But the notion of fairness is far from universal. It varies from person to person and shifts from one context to another. In terms of co-ownership, let’s think of it as a function of:

- Objective factors, such as individual contributions

- The relative value assigned to each objective factor

Preferences

Individual co-owners may come to this decision-making process with a preference for how to divide ownership. Experiences, beliefs, and values play a role. Because preferences are personal and evolve, they’re not always easy to recognize or articulate.

Unique considerations

Sometimes co-owners have a situation that doesn’t fit neatly into a box. We’ve seen instances where one person’s contribution makes all the difference. For example, one co-owner may contribute a relatively greater amount towards the down payment. If this contribution is essential to the group’s ability to qualify for a mortgage, the practical value may exceed the dollar amount.

Other things to think about

Shared motivations and goals

Motivations and goals for co-ownership vary from person to person. In the context of homeownership, goals are similar to preferences: they’re highly personal and dynamic. Many folks find it tough to articulate and confirm alignment around their goals for co-ownership.

When co-owners have different objectives, there tends to be more friction around how to split ownership. These differences may pose a challenge to successful co-ownership.

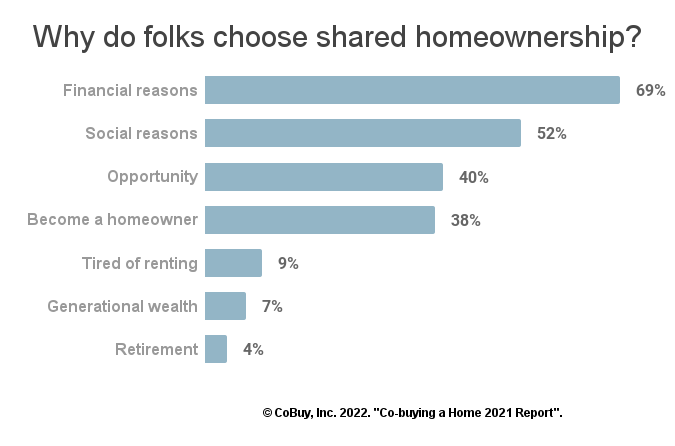

💡 Fast Fact

Financial reasons and social reasons are the top drivers behind the decision to buy and own a home together.

Implications for Title

How you decide to split ownership interest in the property has implications for structuring ownership. Specifically, it impacts how you’re able to take and hold Title to the property.

🔤 Definitions

Title conveys ownership interest in real property and is reflected in a written, recorded document called a Deed. Co-owners who choose to divide ownership interest unevenly often take and hold Title as Tenants in Common.

Tenancy in common (TIC) "is a form of concurrent estate in which each owner, referred to as a tenant in common, is regarded by the law as owning separate and distinct shares of the same property. By default, all co-owners own equal shares, but their interests may differ in size." Source: Wikipedia

Co-ownership agreement

Once you’ve agreed on key aspects of the co-ownership arrangement, like how to split ownership and how you’ll take Title, you need to document these decisions in a written co-ownership agreement. You’ll also want to record your agreement with your local jurisdiction.

Tax and accounting

How you decide to split ownership in the property and structure co-ownership has implications for taxes and accounting. The actions you take can affect the tax status of the jointly owned property, your personal tax treatment, and eligibility for deferral of capital gains tax under a 1031 exchange. You should also be aware of tax implications upon sale.

"There is no gain or loss to recognize on property transfers between spouses. For other individuals, sales of property (including the sale of a partial interest) are taxable events. The Sec. 121 gain exclusion does apply to the sale of a partial interest in a home, so it may offset part or all of the tax."

⚠️ Caution

Attempts to circumvent taxes on the transfer of wealth will result in a call from the IRS.

Example:

Imagine a situation where two sisters co-buy a home for $700,000 with financial assistance from their grandmother. If Grandma contributes $500,000 towards the down payment but takes an equity stake of just 3% in the home, the tax authorities will have questions.

Splitting ownership is just one piece

Align on finances, structure, and goals — before you commit.

Get your CoBuy Decision Brief™ →

$250 per group

Why co-owners should use a top-down approach

With so many variables, what’s the best way to tackle splitting ownership in a home? We recommend a top-down approach. This method involves getting on the same page about the big picture first. Co-owners start by defining who will be involved, what each party will contribute, and shared goals. From there, co-owners progressively drill down into the details.

Why use a top-down approach? It’s systematic, and it ensures that you:

- Cover your bases

- Focus on what’s relevant

- Identify challenges/issues

In short, it’s efficient and effective. We’ve used it with all our past CoBuyers and in our own personal situations.

⭐️ Pro tips

✅ Get expert support

✅ Understand how you hold Title

✅ Use a top-down approach

❌ Don’t underestimate the risks of winging it

Your home, relationship(s), and investment are worth protecting.

Bottom line

Teaming up to buy and own a home speeds path to homeownership, increases purchasing power, and cuts costs. On a human level, co-ownership appeals to our social nature. Since co-owners share mutual interests, a shared plan for success makes sense.

In this post, we’ve looked at a basic framework for how to split ownership in a home. Our experience at CoBuy suggests that a process-driven, methodical approach creates ideal conditions for informed decision making. It sterilizes topics that may otherwise feel uncomfortable to discuss and reduces competitive anxiety between people who care about one another. The resulting clarity helps everyone feel good about co-ownership.

Turn ownership decisions into a plan

Agreements, equity tracking, expenses, and exit strategy — one platform.

Get your Co-ownerOS™ Annual Pass →

$1,000/year per group · Agreement, expenses, equity, exit planning

Check out our other posts: