Co-buying & Co-owning a Home 2026 National Report

The state of co-buying and co-ownership in 2026. 31.5% of U.S. home purchases involve co-buyers. 64M Americans co-own a home. CoBuy's 2026 national report.

Written by Matt Holmes, Pam Hughes, Team CoBuy

CoBuy's Fifth National Report

The state of co-buying and co-ownership in the United States. Data, trends, and findings based on more than 6,200 co-buyers and co-owners. If you're planning to buy with others or already own together, this is your data.

⚡️ Key takeaways

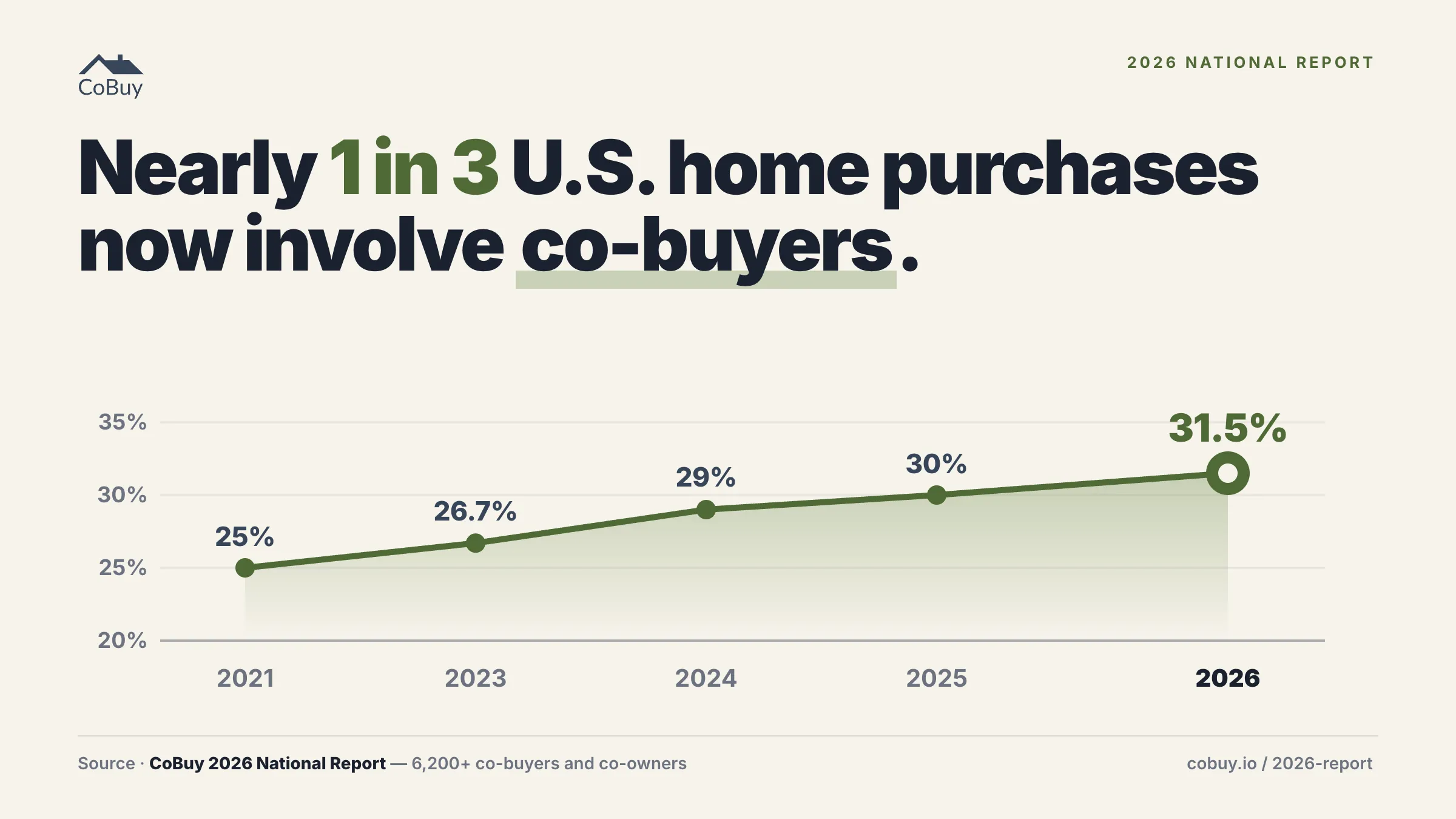

• 31.5% of U.S. home purchases now involve co-buyers. 64 million Americans co-own a home with someone they're not married to.

• Friends are the #1 co-buying aspiration. They are not the #1 co-ownership outcome. A 15-point drop between planning and ownership.

• Co-buyers need far more help than co-owners with legal questions. A 21-point gap, the largest across every support category.

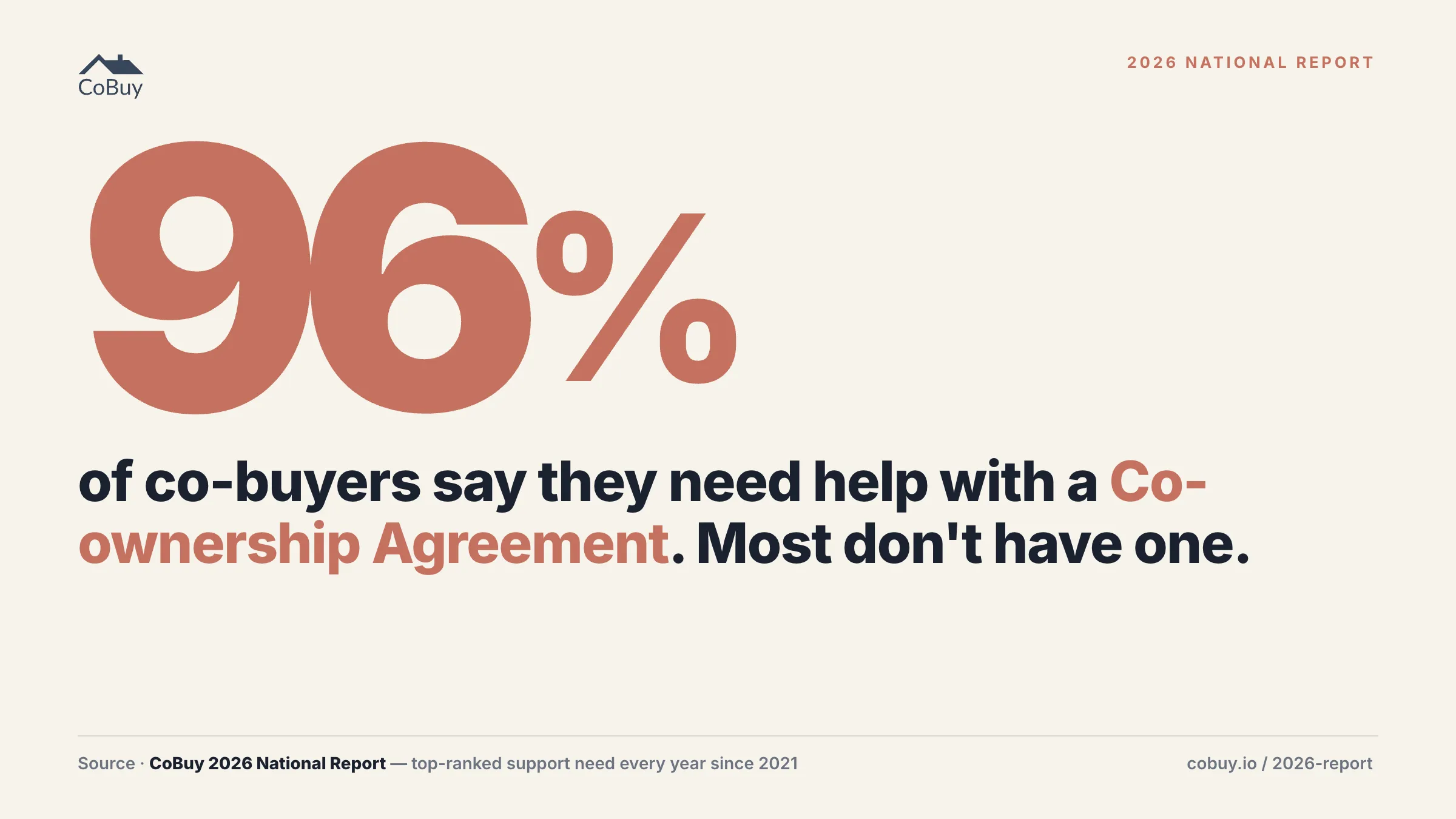

• 96% of co-buyers need help with their Co-ownership Agreement. It has topped the list in every CoBuy report since 2021.

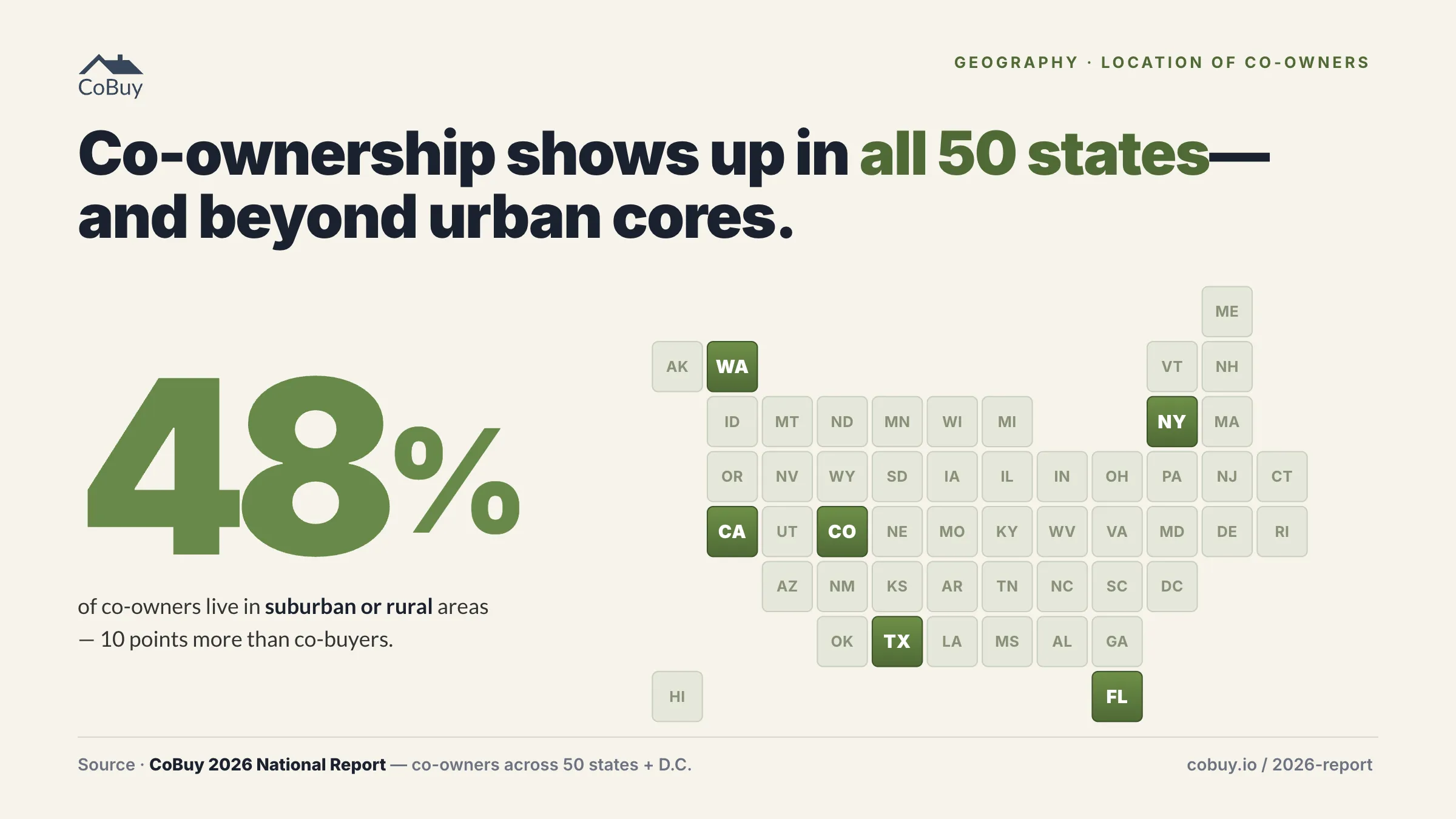

• Co-ownership extends beyond urban cores. Nearly half of co-owners live in suburban or rural areas across all 50 states.

• Co-buying is not a response to one market condition. The same motivations (financial, social, desire to own) have ranked #1, #2, and #3 for five years running.

Co-buying and co-ownership by the numbers

31.5% of U.S. home purchases now involve co-buyers, and 64 million Americans co-own a home with someone they're not married to.

The average co-owner group includes 3.7 people.

These estimates extend a trend line CoBuy has tracked since 2021, when we published the first national report on co-buying and co-ownership. Five years of data tell a consistent story.

| Metric | 2021 | 2023 | 2024 | 2025 | 2026 |

|---|---|---|---|---|---|

| Co-buyer share of home purchases | 25.0% | 26.7% | 29.0% | 30.0% | 31.5% |

| Total co-owners (millions) | 50M+ | 53M | 58M | 61M | 64M |

| Average group size | 3.3 | 3.3 | 3.3 | 3.6 | 3.7 |

Co-buying's share of the housing market has grown from one in four to nearly one in three. The number of Americans co-owning homes has increased by 14 million. Average group size held steady at 3.3 for three consecutive years before breaking out to 3.6 in 2025 and reaching 3.7 in 2026. Multi-generational households are at record levels.

This is not a trend. It is a structural shift in how Americans access homeownership.

⚡️ See where you fit

Take CoBuy's free 1-minute Co-ownership Snapshot. Compare your situation to 6,200+ co-buyers and co-owners. No signup required.

And yet, the systems that support homeownership have not caught up.

Mortgage underwriting is designed for a single borrower or a married couple. Title structures default to individual or spousal joint tenancy. Legal frameworks for residential property were designed for nuclear households. Tax regimes, insurance products, and estate planning tools follow the same assumption: a home is owned by one person or one married couple.

For 64 million Americans, none of this fits.

No one wakes up and calls themselves a co-buyer. But co-buyers account for 31.5% of home purchases. And still, co-buyers and co-owners struggle because the system has major gaps and fundamental flaws.

The result is what we call the Infrastructure Gap: the distance between how people actually buy and own homes and what the systems around them support. We started CoBuy because we decided to co-buy a home together, as mother and son. The process was harder than either of us expected, and we're finance and real estate professionals. That's why we built this company. This report maps the specific dimensions of that gap, drawing on CoBuy's proprietary data from a decade of working with co-buyers and co-owners, four prior annual surveys, and analysis of federal housing data. CoBuy's research on co-buying and co-ownership has been cited by The New York Times, The Wall Street Journal, Forbes, TIME, and more than 20 other publications.

Previous reports: 2021 | 2023 | 2024 | 2025

The Aspiration Gap: Why Most Co-Buying Groups Never Close

Not everyone who plans to co-buy makes it to co-ownership. The groups that aspire to buy together and the groups that actually sustain shared ownership are not the same groups.

Friends are the #1 co-buying aspiration. They are not the #1 co-ownership outcome.

Among co-buyers in CoBuy's dataset, 61% say they are buying with friends. Among co-owners, that number drops to 46%. A 15-point gap between the planning stage and the ownership stage.

Family tells the opposite story. Among co-buyers, 33% include family members. Among co-owners, that rises to 37%. Partners, both married and unmarried, hold steady across both stages.

This pattern is not new. CoBuy's 2023 report first identified it: "The proportion of groups that include friends is lower for co-owner groups vs co-buyer groups... a function of the aspirational nature of co-buying." Multiple years of data across independent sources confirm it.

💡 Our read

The mechanics behind the aspiration gap aren't mysterious. The co-buying process is emotional and social. The co-ownership that follows is operational and financial. Friend groups over-index on the first and under-index on the second.

Family and partners bring pre-existing infrastructure that friend groups start without: shared finances, shared estate planning, existing legal ties, and long-term geographic gravity. None of that is automatic for friends. It has to be built deliberately, against time pressure.

Friends also disperse. Jobs change. Relationships change. Cities change. The friends sitting around a kitchen table imagining a house together aren't always the same friends still in the same city two years later when a property comes up.

This is not a judgment. Friends remain the largest co-buying segment. More friend groups attempt co-buying than any other type. The aspiration gap is real, but friends are still the dominant starting point.

Curious which segment you and your group fall into? The free Co-ownership Snapshot compares your situation to 6,200+ others in about a minute.

The same dynamic appears in group size. Some co-buyers aspire to larger groups: roughly one in six plans to buy with five or more people. In our experience, 95% of groups with six or more members do not complete a home purchase together. They split, downsize, or decide not to move forward.

More than 60% of co-buying groups who set out to purchase a home together never complete the process.

Every type of group needs structure. Family, friends, couples, mixed groups: none of them come with a built-in framework for shared property ownership. But the data is clear that friend groups are more likely to start the process and less likely to finish it. The aspiration is not the problem. The absence of structure is.

Co-buying without structure is like starting a business without an operating agreement. The groups that succeed are the ones that plan for disagreement before it arrives, and actively manage their shared investment over time.

What Co-buyers and Co-owners Need

Co-ownership Agreement topped the list of what co-buyers and co-owners need help with in CoBuy's 2021, 2023, 2024, and 2025 reports. In 2026, it remains #1 for the fifth consecutive report.

96% of co-buyers say they need help with their Co-ownership Agreement. Most don't have one.

CoBuy's 2023 report first split this data by stage. The 2026 dataset deepens that analysis with a larger and more recent sample of co-buyers (those planning a purchase) and co-owners (those who already own together). The gap between the two reveals where the Infrastructure Gap is widest, and where it persists even after purchase.

| Category | Co-buyers | Co-owners | Gap |

|---|---|---|---|

| Co-ownership Agreement | 96% | 82% | +15 |

| Finances, payments, expenses | 74% | 67% | +7 |

| Legal | 73% | 52% | +21 |

| Roles, rights, responsibilities | 72% | 61% | +11 |

| Documentation and record-keeping | 69% | 68% | +1 |

| Exit strategy | 65% | 51% | +15 |

| Tax and accounting | 65% | 55% | +10 |

| Risk protection | 63% | 52% | +11 |

| Admin | 51% | 51% | 0 |

| Scheduling | 40% | 39% | +1 |

Based on CoBuy's 2026 dataset of co-buyers and co-owners across all 50 states.

Three years of pain point rankings show remarkable stability. Co-ownership Agreement has been #1 every year. The top six categories have barely reshuffled. The specific numbers move within narrow bands. The structural picture does not change.

| Category | 2024 | 2025 | 2026 |

|---|---|---|---|

| Co-ownership Agreement | 90% | 94% | 91% |

| Finances, payments, expenses | 73% | 69% | 71% |

| Documentation and record-keeping | 69% | 66% | 69% |

| Roles, rights, responsibilities | 68% | 66% | 68% |

| Exit strategy | 58% | 63% | 60% |

| Risk protection | 56% | 59% | 58% |

Sample sizes: 2024 (1,954 adults across 601 groups), 2025 (1,637 adults across all 50 states), 2026 (CoBuy's dataset of co-buyers and co-owners, all 50 states). CoBuy's 2021 report used different category names but found the same top challenge (88% needing help with the co-buying process). The 2023 report reported 94% needing help overall.

Co-buyers need more legal help than co-owners by 21 percentage points, the largest gap across all categories. Exit strategy and Co-ownership Agreement each show a 15-point gap. Risk protection and roles/responsibilities show 11-point gaps.

The pattern is clear: co-buyers are navigating unknowns. Co-owners have partially figured things out through experience. The gaps in legal, exit, and agreement needs narrow after purchase as co-owners learn by doing.

But some challenges do not fade. Documentation and record-keeping (+1 point) and admin (0 points) are flat across both groups. The operational grind of shared homeownership, tracking expenses, managing records, coordinating logistics, persists regardless of whether you bought last month or five years ago. For groups that already own together, Co-ownerOS™ provides the structure for this stage: agreements, finances, documentation, and exit planning in one place. $1,000/year per group.

The infrastructure gap narrows after purchase. It doesn't fully close.

The traditional path to creating a Co-ownership Agreement through an attorney costs $10,000 to $15,000 or more. Most co-owner groups don't have one. They don't know they need one, they can't find an attorney with co-ownership experience, or the $10,000-to-$15,000 price tag stops them cold. Without one, co-owners face up to $765,000+ in cumulative financial risk over ten years. Or worse: a $350,000 disaster that could have been prevented with a few structured conversations and a written agreement.

96% of co-buyers say they need help with their Co-ownership Agreement. The CoBuy Decision Brief™ gives your group a structured assessment of where you stand and what to do next. $250 per group.

Who Co-owns Homes

There is no typical co-owner. Co-ownership attracts people across every age group, income level, and geography, united by a shared decision to buy or own property with someone they are not married to.

The data challenges several common assumptions.

Co-buying is not only a young person's strategy

One in four co-buyers is over 40. Ages in CoBuy's data span the mid-20s to the late 80s. Co-buying is not concentrated in any single generation.

This is not how co-buying is typically covered. Media attention centers on younger friends. The over-40 cohort is under-reported and underestimated, even as multi-generational arrangements reach record highs.

Over 65 million Americans now live in multi-generational households. An estimated $124 trillion in assets will change hands over the next two decades, according to Cerulli Associates, much of it in real estate. As demographics shift, more families are pooling resources across generations. Co-buying is one of the primary vehicles for this.

Most co-buyers are financially qualified

Co-buyers span every income level. This is not a last-resort strategy for people who cannot qualify individually. Among co-buyers on CoBuy's platform, nearly half have household incomes above $100,000. 93% report credit scores above 700. The median co-buying budget is nearly $700,000.

These are financially capable households choosing co-ownership because it offers better access, better economics, or a better fit for how they want to live. Many more households are financially qualified than realize it: teaming up unlocks purchasing power individual buyers can't access alone. See what your group can afford with our budget calculator.

Co-buying is a long-term housing strategy

72% of co-buying groups on CoBuy's platform are purchasing a primary residence. 31% plan to co-own for 10 or more years. 80% plan to live in the home.

Co-ownership is not a stepping stone. For most groups, it is the plan.

Geography

Co-ownership spans all 50 states and Washington, D.C. The top states in CoBuy's data are California, Washington, New York, Texas, Florida, and Colorado.

Co-ownership is not exclusively urban. In CoBuy's data, roughly 4 in 10 co-buyers and nearly half of co-owners are in suburban and rural areas. Co-owners are about 10 percentage points more likely to be in non-urban locations than co-buyers, a pattern consistent with the aspiration gap: co-buying interest concentrates in cities, but co-ownership materializes across a broader geographic range.

Motivations

The top motivations for co-buying have remained consistent across all five annual reports:

- Financial reasons

- Social reasons

- Desire to own

Financial. Co-buying distributes the down payment, the mortgage, the upkeep, and the tax burden across multiple parties. It unlocks access to properties, neighborhoods, and equity that individual budgets can't reach.

Social. Household formation has changed. More adults live with other adults, by choice. Multi-generational arrangements, chosen family, close friends. Co-ownership is the property structure that matches how people actually live.

Desire to own. Co-buyers aren't compromise buyers. They aren't co-buying because they gave up on owning. They're co-buying because it gets them to ownership. The goal is the same as any other buyer: a place of your own, long-term equity, housing security.

The rank order has not changed since 2021. Five years, five reports, the same three motivations in the same order. The consistency itself is the finding: co-buying is not a response to a single market condition. It persists across rate environments, price cycles, and economic shifts. Co-buying increases purchasing power by distributing costs across the group while providing access to properties and neighborhoods that would be out of reach individually.

Group composition

The average co-owner group includes 3.7 people. Groups include friends, family members, unmarried couples, married couples alongside other co-owners, and mixed groups that span more than one relationship type.

The Alignment Problem: The Conversations Most Groups Skip

Before anyone looks at a property, a substantial share of co-buying groups have not resolved the most basic terms of their arrangement.

Among co-buying groups in CoBuy's platform data, 44% plan to split ownership evenly. 24% plan uneven splits. Nearly one-third are undecided.

The same pattern holds for timeline:

- 31% plan to co-own for 10 or more years.

- Almost 30% have not decided how long they plan to co-own together.

Ownership split and co-ownership horizon are the two most consequential decisions a co-buying group makes. They determine how equity is allocated, how expenses are divided, how buyouts are priced, and what happens when someone wants out. When these questions go unanswered, groups do not disagree. They stall.

Here's what that looks like in practice.

Take a common structure: two couples, multi-generational. Parents in their 60s bring cash from a home sale. Adult children bring strong borrowing power but less liquidity. Target property around $2 million. The parents put up the down payment. The younger couple carries the mortgage. On paper, clean.

In practice, the question dominates every conversation: what does "fair" look like when cash and borrowing power are different currencies? Does the couple putting up cash take a larger share because more capital is at risk? Does the couple carrying the 30-year mortgage take a larger share because they carry the obligation? Is it 50/50 with an equalization at sale? Proportional to monthly contribution?

💡 Our read

Every answer has trade-offs. No answer is wrong. Without a structured way to surface preferences, quantify trade-offs, and document decisions, the group stalls. Not from conflict. From the absence of a method.

The data shows this at every stage. The vast majority of co-buying groups on CoBuy's platform never involve their co-buyers in the process. They sign up, explore, and stop before inviting anyone else. The process does not break down from conflict. It breaks down from the absence of a structured way to start the conversation.

This is the Alignment Problem: the gap between wanting to co-buy and knowing how to align with the people you plan to do it with. It explains why 96% need help with Co-ownership Agreements, why 72% need help defining roles and responsibilities, and why 65% need help with exit strategy. These are not administrative tasks. They are alignment questions. Who owns what. Who does what. What happens when circumstances change.

Thousands of co-buyer and co-owner groups have asked us about legal agreements and structuring, family and multi-generational arrangements, and a question that hits on the Infrastructure Gap in four words: "How does it work?"

The groups that make it through are the ones that answer these questions early, in writing, before they commit capital.

The CoBuy Decision Brief™ surfaces the conversations most groups skip. It assesses your group's alignment across finances, ownership structure, and co-ownership terms, and gives you a clear picture of where you stand before you commit. $250 per group.

Methodology

CoBuy pioneered research on co-buying and co-ownership, publishing the first national report on the category in 2021. This is CoBuy's fifth national report. Across the series, CoBuy's research spans more than 6,200 co-buyers and co-owners across all 50 U.S. states and Washington, D.C.

The 2026 headline figures (31.5% co-buyer share of U.S. home purchases, 64 million co-owners, 3.7 average group size) are produced by CoBuy's proprietary estimation model. The model combines federal housing data from the U.S. Census Bureau's American Community Survey and the Consumer Financial Protection Bureau's Home Mortgage Disclosure Act with ten years of CoBuy's platform data. The same model has been applied across every report in the series.

Findings on group composition, pain points, motivations, ownership structure, and geography are drawn from two proprietary datasets: platform data covering thousands of co-buying groups, and waitlist surveys representing more than 3,400 individuals. Both datasets are national in scope and self-selected. Neither is a nationally representative random sample. Findings are scoped accordingly.

Historical findings are cited independently by year and not pooled. Prior samples: 2021 (476 adults), 2023 (1,419 adults), 2024 (1,954 adults across 601 groups), 2025 (1,637 adults across all 50 states).

Give Your Group the Structure It Needs

Co-ownership is how millions of Americans buy and own homes. The question is not whether it works. It is whether the tools exist to make it work well.

Not sure where you fit yet?

See how your situation compares to 6,200+ co-buyers and co-owners.

Take the 1-minute Snapshot →

Free · No signup

Co-buyers: start here.

Align on finances, ownership, and exit before you commit.

Get your CoBuy Decision Brief™ →

$250 per group

Co-owners: run it like a team.

Agreements, expenses, equity, exit planning.

Get your Co-ownerOS™ Annual Pass →

$1,000/year per group · Agreement, expenses, equity, exit planning

FAQs

What is a co-buyer?

A co-buyer is anyone who purchases a home with someone who is not their spouse. Co-buyers become co-owners at closing.

How many Americans co-own a home?

Over 64 million Americans co-own a home with a non-spouse as of 2026. Co-buyers represent 31.5% of all U.S. home purchases, up from 25% in 2021.

What types of groups co-own homes?

Friends, family members, unmarried couples, married couples alongside other co-owners, and mixed groups. The average group size is 3.7 people. Co-ownership spans all 50 states and all age groups.

What are the biggest challenges co-buyers and co-owners face?

Co-ownership Agreement (96% of co-buyers need help), finances and expenses (74%), legal questions (73%), roles and responsibilities (72%), documentation (69%), and exit strategy (65%).

Do co-owners need a Co-ownership Agreement?

Yes. A Co-ownership Agreement defines ownership structure, financial terms, roles, and what happens when circumstances change. Without one, there is no framework for disagreements, financial changes, or exits. 96% of co-buyers and 82% of co-owners say they need help with this. The traditional path through an attorney costs $10,000 to $15,000 or more.

What happens if a co-owner wants to sell?

Without a Co-ownership Agreement, any co-owner can force a sale through a partition action, which can cost $75,000 or more and take 18 months or longer. A proper exit strategy defines buyout pricing, right of first refusal, and timelines before they are needed.

Is co-buying only popular in expensive cities?

No. CoBuy's data spans all 50 states and Washington, D.C., across urban, suburban, and rural areas. The top states by concentration are California, Washington, New York, Texas, Florida, and Colorado.

Fair Use

If you would like to feature, reference, or reproduce any portion of this report, you have our permission subject to clear attribution to CoBuy and a dofollow link to either https://www.cobuy.io or this page's URL.

Related posts:

- Co-ownership Agreement: What to Include and Why

- TIC vs JTWROS: which title structure is right?

- Co-ownership Exit Strategies

- Co-ownership Insurance

- Documentation in Co-ownership

- Hidden Costs of Co-ownership

- The $350,000 Co-ownership Disaster

- Buy a Home with Family Members

- Co-own a Home with an Unmarried Partner

- The Ultimate Guide to Shared Homeownership

Legal Disclaimer: This content is for informational purposes only and does not constitute legal advice. Co-ownership laws and practices vary by jurisdiction. For specific legal concerns, consult a qualified attorney.